Executive Credit Risk Dashboard

Portfolio Performance & Risk Monitoring Framework

This dashboard simulates the risk monitoring framework of a fintech specialized in unsecured personal loans. It provides a structured view of portfolio risk, borrower profile segmentation, pricing dynamics and default behavior.

Model Development – Probability of Default (PD)

Key Insights & Strategic Findings

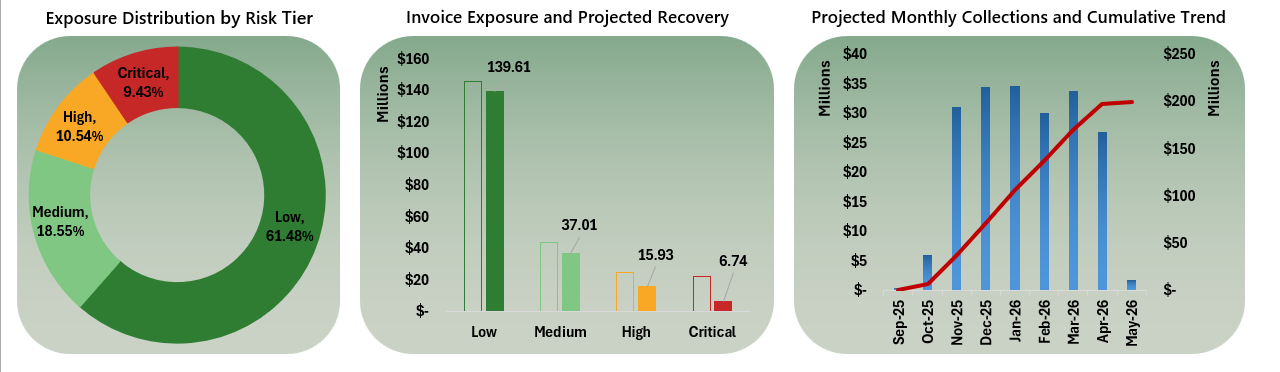

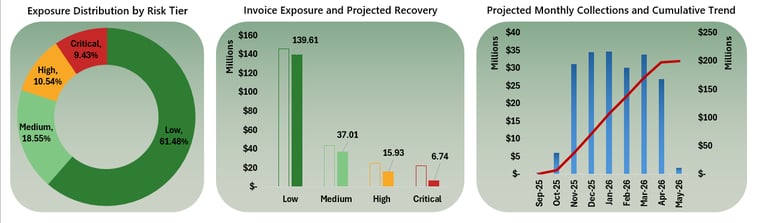

80% of the portfolio falls within low and medium risk levels, with less than 10% concentrated in the critical risk segment, reflecting a largely healthy portfolio with clear opportunities for preventive risk management

The portfolio shows an expected recovery rate of 84%, allowing anticipation of potential cash flow pressure

The projection indicates that the greatest cash flow erosion is concentrated within the critical segment, enabling prioritization of collection efforts and adjustment of cash flow forecasts accordingly

The cumulative curve shows a relatively steady progression of expected inflows, with no extreme concentration risk in a single month, supporting predictable liquidity planning. 64% of projected cash inflows occur between Jan–Apr 2026

The portfolio presents a total exposure of 236M, of which approximately 37M is classified as expected risk according to the predictive model. This represents nearly 16% of the total portfolio. The tool enables prioritization of this critical segment and allows estimation of its impact on monthly cash flow.

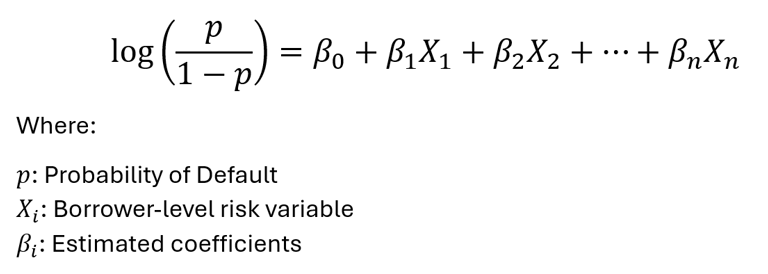

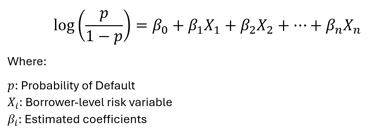

The objective of this model was to estimate the Probability of Default (PD) for unsecured personal loans using borrower-level demographic, financial and credit behavior variables.

The model was designed to:

Support risk-based pricing decisions

Enhance underwriting criteria

Improve expected loss estimation

Enable portfolio risk segmentation

Given the unsecured nature of the lending structure, accurate PD estimation becomes the primary driver of credit risk management.

Methodology – Logistic Regression

A Logistic Regression model was implemented to estimate default probability.

Logistic regression is particularly suitable for credit risk modeling because:

The dependent variable (default vs non-default) is binary

It produces interpretable coefficients

Outputs are directly expressed as probabilities (0–1 range)

It is widely accepted in regulated financial environments

Mathematically, the model estimates the log-odds of default as a linear combination of explanatory variables:

Feature Engineering

Several transformations were applied to enhance predictive signal:

Income segmentation into brackets (low / middle / high)

Encoding of loan grade categories

Historical default flag construction

Standardization of continuous financial variables where necessary

Verification of employment length and credit history consistency

Categorical variables were appropriately encoded to preserve economic interpretability.

Variable Selection

Variables were selected based on:

Economic intuition

Statistical significance

Multicollinearity assessment

Contribution to model stability

Key predictive variables included:

Loan grade

Interest rate

Historical default indicator

Employment length

Credit history length

Income segment

Loan intent

Exploratory Data Analysis (EDA)

Before formal model development, a structured Exploratory Data Analysis (EDA) was conducted to:

Understand borrower risk distribution

Identify preliminary risk drivers

Detect data inconsistencies

Validate economic relationships between variables

Support feature engineering decisions

The EDA phase served as the analytical foundation for the Probability of Default (PD) model.

Defaulted Loans Global Distribution

Defaulted Loans Age Distribution

Defaulted Loans Income Distribution

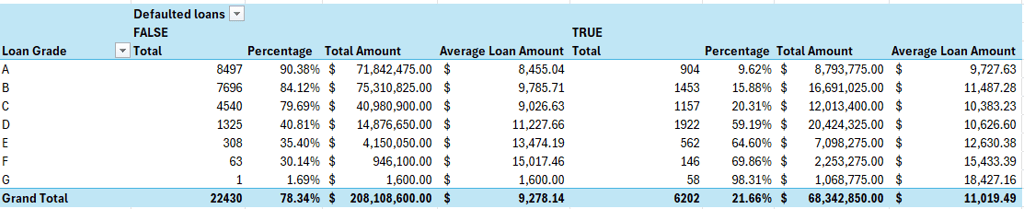

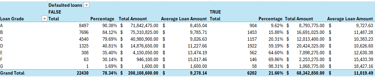

Defaulted Loans Grade Distribution

Defaulted Loans Historical Distribution